'Lessons in private-private financial information sharing to detect and disrupt crime'

A Survey and Policy Discussion Paper

Nick J Maxwell, July 2022

This survey of both AML and fraud prevention private-private information-sharing platforms explores 15 different initiatives across the United States, the United Kingdom, Singapore, the Netherlands, Switzerland, Estonia and Australia.

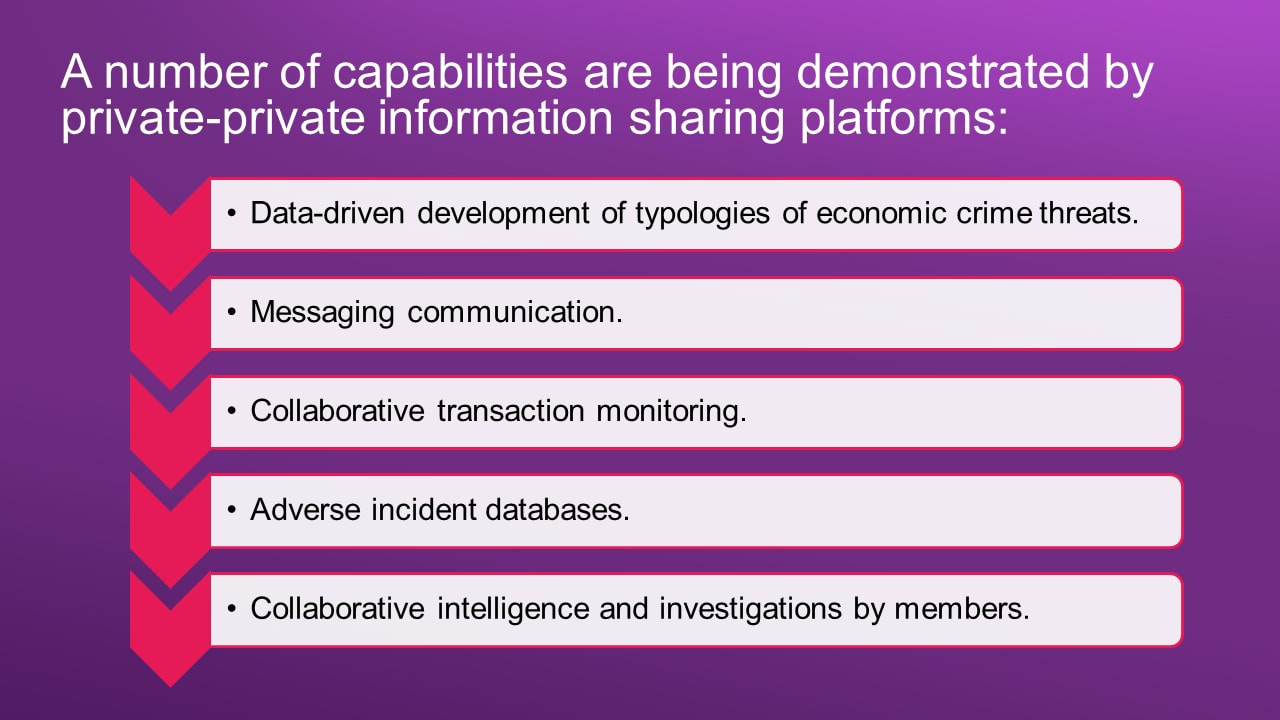

The survey identifies that various capabilities are being demonstrated by platforms - from data-driven development of economic crime typologies, to joint transaction monitoring, to adverse databases, to joint investigations, to messaging capabilities.

The survey identifies that various capabilities are being demonstrated by platforms - from data-driven development of economic crime typologies, to joint transaction monitoring, to adverse databases, to joint investigations, to messaging capabilities.

DOWNLOAD THE FULL REPORT

| rusi_ffis_survey_and_policy_discussion_paper_-_lessons_in_private-private_financial_information_sharing_to_detect_crime.pdf |

The survey is not intended to be exhaustive, but will be updated in future iterations as more platforms are surveyed. In its current form, the study collates performance information for those 15 platforms and reviews a number of policy and data protection issues relevant to the field. We describe how the platforms vary in terms of the capabilities they offer, the data they ingest, the data they provide to members, the legal framework they operate in, what impact or performance information they record, how they engage with public authorities, how they communicate with data subjects and what interaction they have with financial exclusion issues.

Key insights of the report:

Private-private information sharing to detect economic crime is accelerating around the world, with seven out of the 15 platforms surveyed being established since 2020. Recent innovation is occurring in the U.S., the Netherlands, Singapore and Estonia.

Early indicators of impact include the following:

- Transactie Monitoring Nederland (TMNL) (a joint transaction monitoring utility between five major Dutch banks) has contributed to 85% time-saving efficiency gains in financial intelligence tasks.

- Innovation in the U.S., through the Collaborative Investigations Model, has demonstrated that – when initiated by a law enforcement case – private sector collaboration can identify, on average, 5 times the number of subjects related to a potential money laundering network than were originally known to law enforcement investigators.

- Other innovations in the U.S. are demonstrating that, through the use of privacy enhancing technology, queries can take place to consortiums of financial institutions, without the details of the query being disclosed in the process and response times are being reduced to automated and instant replies, compared to previous processes that took weeks or months to receive replies.

- Fraud-prevention platforms in the UK are leading to billions of pounds (GBP) of loss to fraud being identified and prevented.

Innovation is occurring in different ways – for example – the U.S. is seeing innovation in the use of privacy enhancing technology and joint investigations; Singapore is creating a shared database of clients that are exited for financial crime reasons; and the Netherlands is allowing for joint transaction monitoring and analytics over connected transaction data.

We observe that significant strides forward have taken place in resolving data inter-operability issues between private-sector entities so as to link respective datasets and that (in the EU context) the EU General Data Protection Regulation (GDPR) is not, prima facie, a barrier to such platforms operating.

However, the paper also observes that many of the platforms are stymied by an unclear policy and regulatory environment that does not provide for a specific enabling legal basis for the information-sharing, contributing to various limiting effects.

The final section of the study sets out three enabling themes and 15 key contributing factors which aim to serve policy consideration about how to support the growth of private-private financial information-sharing capabilities in a secure, effective and efficient manner that meets both data protection and economic crime policy needs.

This research paper has been supported by Synectics Solutions and supplemented by grant funding by the SWIFT Institute.

We observe that significant strides forward have taken place in resolving data inter-operability issues between private-sector entities so as to link respective datasets and that (in the EU context) the EU General Data Protection Regulation (GDPR) is not, prima facie, a barrier to such platforms operating.

However, the paper also observes that many of the platforms are stymied by an unclear policy and regulatory environment that does not provide for a specific enabling legal basis for the information-sharing, contributing to various limiting effects.

The final section of the study sets out three enabling themes and 15 key contributing factors which aim to serve policy consideration about how to support the growth of private-private financial information-sharing capabilities in a secure, effective and efficient manner that meets both data protection and economic crime policy needs.

This research paper has been supported by Synectics Solutions and supplemented by grant funding by the SWIFT Institute.